Enter name(s) as shown on Form 740, page 1. Your Social Security Number

KENTUCKY ITEMIZED DEDUCTIONS

FULL-YEAR RESIDENTS ONLY

Enclose with Form 740

2021

740

SCHEDULE A

Commonwealth of Kentucky

Department of Revenue

FORM

Interest

Expense

Other

Miscellaneous

Deductions

Total

Itemized

Deductions

Contributions

Note:

For any contri-

bution of $250

or more, see

instructions.

DIVIDING DEDUCTIONS BETWEEN SPOUSES

Use this schedule if married filing separately on a combined return.

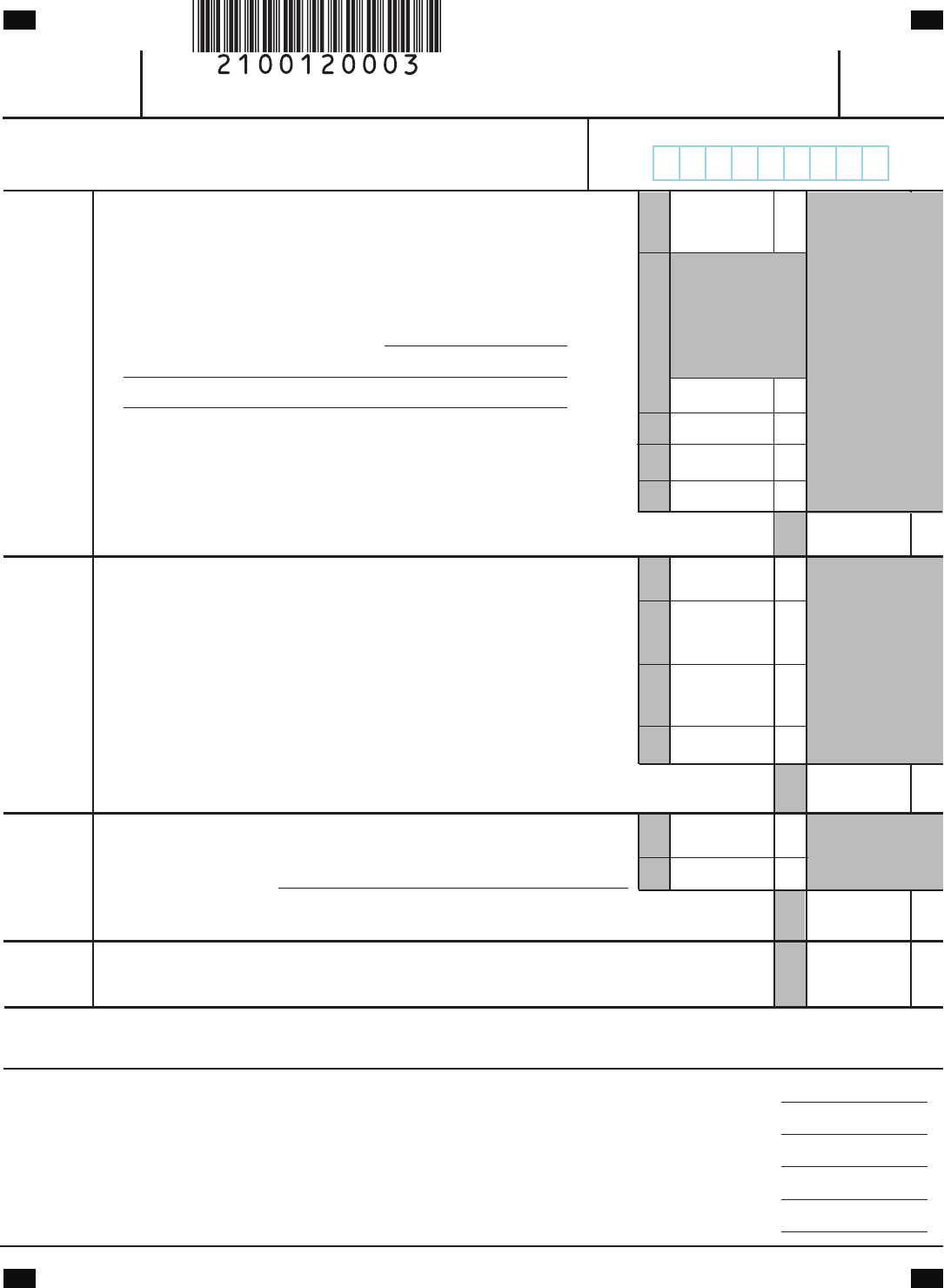

16 Total itemized deductions, line 15 .................................................................................................................................... .00

17 Percent of income (Form 740, line 9, Column A) to total income (Form 740, total of line 9, Columns A and B) ....... %

18 Percent of income (Form 740, line 9, Column B) to total income (Form 740, total of line 9, Columns A and B) ....... %

19 Percent on line 17 times total deductions entered on line 16 (enter here and on Form 740, line 10, Column A) ..... .00

20 Percent on line 18 times total deductions entered on line 16 (enter here and on Form 740, line 10, Column B) ..... .00

210012 42A740-A (10-21) Page 1 of 5

1 Home mortgage interest and points reported to you on

federal Form 1098 ..................................................................................................... 1 00

2 Home mortgage interest not reported to you on federal

Form 1098 (if paid to an individual, provide that person’s

name, identifying number and address)

2 00

3 Points not reported to you on federal Form 1098 .................................................. 3 00

4 Qualified mortgage insurance premiums .............................................................. 4 00

5 Investment interest (enclose federal Form 4952 if required) ................................ 5 00

6 Total Interest. Add lines 1 through 5. Enter here ................................................................................ 6 00

7 Contributions by cash or check ............................................................................... 7 00

8 Other than cash or check (enclose federal Form 8283

if over $500) .............................................................................................................. 8 00

9 Artistic charitable contributions deduction

(enclose copy of appraisal)...................................................................................... 9 00

10 Carryover from prior year ........................................................................................ 10 00

11 Total Contributions. Add lines 7 through 10. Enter here .................................................................... 11 0 0

12 Gambling losses ...................................................................................................... 12 00

13 Other (see instructions) 13 00

14 Total Other Miscellaneous Deductions. Add lines 12 and 13. Enter here ....................................... 14 00

15 Add lines 6, 11, and 14. Enter here ......................................................................................................... 15 00

Page 2 of 5

You may itemize your deductions for Kentucky even if you do

not itemize for federal purposes. Generally, if your deductions

exceed $2,690, it will benefit you to itemize. If you do not

itemize, you may elect to take the standard deduction of

$2,690.

Special Rules for Married Couples—If one spouse itemizes

deductions, the other must also itemize. Married couples

filing a joint federal return and who wish to file separate

returns or a combined return for Kentucky may: (a) file

separate Schedules A showing the specific deductions

claimed by each, or (b) file one Schedule A and divide the

total deductions between them based on the percentage of

each spouse’s income to total income.

Lines 1 through 6—Interest Expense

You may deduct interest that you have paid during the tax-

able year on a home mortgage. You may not deduct interest

paid on credit or charge card accounts, a life insurance loan,

an automobile or other consumer loan, delinquent taxes or

on a personal note held by a bank or individual.

Interest paid on business debts should be deducted as a

business expense on the appropriate business income

schedule.

You may not deduct interest on an indebtedness of another

person when you are not legally liable for payment of the

interest. Nor may you deduct interest paid on a gambling

debt or any other nonenforceable obligation. Interest paid

on money borrowed to buy tax-exempt securities or single

premium life insurance is not deductible.

Line 1—List the interest and points (including “seller-paid

points”) paid on your home mortgage to financial institutions

and reported to you on federal Form 1098.

Line 2—List other interest paid on your home mortgage and

not reported to you on federal Form 1098. Show name and

address of individual to whom interest was paid.

Line 3—List points (including “seller-paid points”) not

reported to you on federal Form 1098. Points (including loan

origination fees) charged only for the use of money and paid

with funds other than those obtained from the lender are

deductible over the life of the mortgage. However, points

may be deducted in the year paid if all three of the following

apply: (1) the loan was used to buy, build or improve your

main home, and was secured by that home, (2) the points

did not exceed the points usually charged in the area where

the loan was made, and were figured as a percentage of the

loan amount, and (3) if the loan was used to buy or build the

home, you must have provided funds (see below) at least

equal to the points charged. If the loan was used to improve

the home, you must have paid the points with funds other

than those obtained from the lender.

Funds provided by you include down payments, escrow

deposits, earnest money applied at closing, and other

amounts actually paid at closing. They do not include

amounts you borrowed as part of the overall transaction.

Seller-Paid Points—If you are the buyer, you may be able to

deduct points the seller paid in 2021. You can do this if the

loan was used to buy your main home and the points meet

item 2 above. You must reduce your basis in the home by

those points, even if you do not deduct them.

If you are the seller, you cannot deduct the points as interest.

Instead, include them as an expense of the sale.

This generally does not apply to points paid to refinance your

mortgage. Federal rules apply. See federal Publication 936

for more information.

Line 4–

Qualified Mortgage Insurance Premiums—

Premiums

that you pay or accrue for “qualified mortgage insurance”

during 2021 in connection with home acquisition debt on

your qualified home are deductible as home mortgage

insurance premiums. Qualified mortgage insurance is

mortgage insurance provided by the Veterans Administration,

the Federal Housing Administration, or the Rural Housing

Administration, and private mortgage insurance. Mortgage

insurance premiums paid or accrued on any mortgage

insurance contract issued before January 1, 2007, are not

deductible.

Limit on amount you can deduct. You cannot deduct your

mortgage insuance premiums if the amount of Form 740, line

9, is more than $109,000 ($54,500 if married filing separately

on a combined return or separate returns) If the amount of

Form 740, line 9, is more than $100,000 ($50,000 if married

filing separately on combined return or separate return), your

deduction is limited and you must use the worksheet below

to figure the deduction.

Instructions for Schedule A

Form 740 (2021)

Schedule A

Page 3 of 5

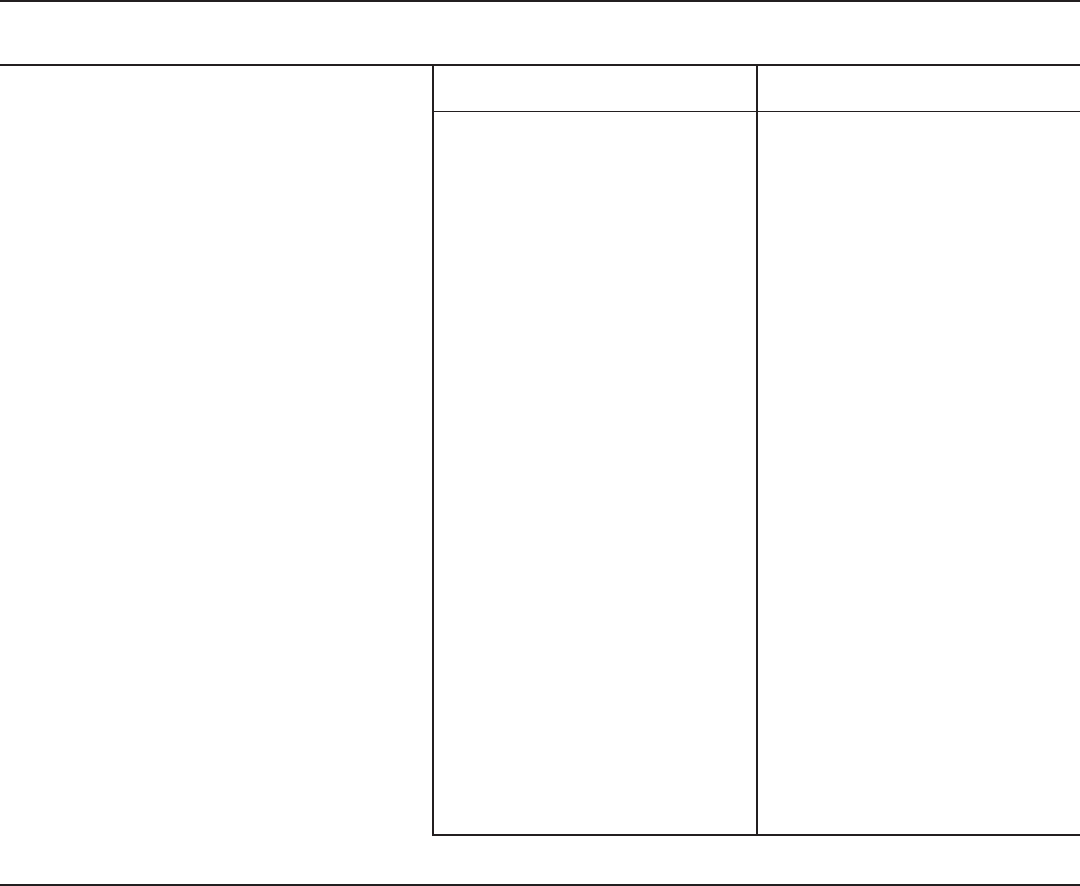

1. Enter the total premiums you paid in 2021

for qualified mortgage insurance for a

contract entered into on or after January 1, 2007 ..... 1. ______________________ 1. _____________________

2. Enter the amount from Form 740, Line 9 ................... 2. _____________________ 2. ____________________

3. Enter $100,000 ($50,000 if married filing

separately on a combined return or

separate returns) ........................................................... 3. _____________________ 3. ____________________

4. Is the amount on Line 2 more than the

amount on Line 3?

No. Your deduction is not limited.

Enter the amount from Line 1 above

on Schedule A, Line 4.

Yes. Subtract Line 3 from Line 2. If the

result is not a multiple of $1,000

($500 if married filing separately on

a combined return or separate returns),

increase it to the next multiple of

$1,000 ($500 if married filing

separately on a combined return or

separate returns). For example,

increase $425 to $1,000, increase

$2,025 to $3,000; or if married filing

separately on a combined return or

separate returns, increase $425 to

$500, increase $2,025 to $2,500, etc. ........... 4. _____________________ 4. ______________________

5. Divide Line 4 by $10,000 ($5,000 if married

filing separately on a combined return or

separate returns). Enter the result as a

decimal. If the result is 1.0 or more,

enter 1.0 ......................................................................... 5. _____________________ 5. ______________________

6. Multiply Line 1 by Line 5 .............................................. 6. ____________________ 6. _____________________

7. Qualified mortgage insurance premiums

deduction. Subtract Line 6 from Line 1 ....................... 7. _____________________ 7. _____________________

8. Add Line 7, Columns A and B. Enter here and

on Schedule A, Line 4 ........................................................................................................................................................ 8. _____________________

A. Spouse B. Yourself (or Joint)

2021 Qualified Mortgage Insurance Premiums Deduction Worksheet

See the instructions for Line 4 above to see if you must use this worksheet to figure your deduction.

Line 5, Interest on Investment Property—Investment

interest is interest paid on money you borrowed that is

allocable to property held for investment. It does not include

any interest allocable to a passive activity or to securities

that generate tax-exempt income.

Complete and enclose federal Form 4952, Investment

Interest Expense Deduction, to figure your deduction.

Exception. You do not have to file federal Form 4952 if all

three of the following apply:

(a) your investment interest is not more than your

investment income from interest and ordinary

dividends,

(b) you have no other deductible investment expenses, and

(c) you have no disallowed investment interest expense

from 2020.

Page 4 of 5

Lines 7 through 11—Contributions

You may deduct what you actually gave to organizations that

are religious, charitable, educational, scientific or literary in

purpose. You may also deduct what you gave to organizations

that work to prevent cruelty to children or animals. In general,

contributions deductible for federal income tax purposes are

also deductible for Kentucky.

Examples of qualifying organizations are:

Churches, temples, synagogues, Salvation Army, Red

Cross, CARE, Goodwill Industries, United Way, Boy

Scouts, Girl Scouts, Boys and Girls Clubs of America, etc.

Fraternal orders if the gifts will be used for the purposes

listed above.

Veterans’ and certain cultural groups.

Nonprofit schools, nonprofit hospitals and medical

research organizations.

Federal, state and local governments if the gifts are solely

for public purposes.

If you contributed to a qualifying charitable organization

and also received a benefit from it, you may deduct only

the amount that is more than the value of the benefit you

received.

Contributions You MAY Deduct

Contributions may be in cash, property or out-of-pocket

expenses you paid to do volunteer work for the kinds of

organizations described above. If you drove to and from the

volunteer work, you may take 16 cents a mile or the actual

cost of gas and oil. Add parking and tolls to the amount you

claim under either method. (Do not deduct any amounts that

were repaid to you.)

Note: You are required to maintain receipts, cancelled checks

or other reliable written documentation showing the name of

the organization and the date and amount given to support

claimed deductions for charitable contributions.

Separate contributions of $250 or more require written

substantiation from the donee organization in addition to

your proof of payment. It is your responsibility to secure

substantiation. A letter or other documentation from the

qualifying charitable organization that acknowledges

receipt of the contribution and shows the date and amount

constitutes a receipt. This substantiation should be kept in

your files. Do not send it with your return.

See federal Publication 526 for special rules that apply if:

your total contributions exceed 60 percent of Kentucky

Adjusted Gross Income,

If a Kentucky Net Operating Loss Deduction (KNOLD) is

present, you must figure your Kentucky Adjusted Gross

income without the KNOLD before applying the 60%

limitation. 740, line 7 less Schedule M, line 15 equals

your Kentucky Adjusted Gross Income without KNOLD.

your total deduction for gifts of property is over $500,

you gave less than your entire interest in the property,

your cash contributions or contributions of ordinary

income property are more than 30 percent of your

Kentucky Adjusted Gross Income,

your gifts of capital gain property to certain organizations

are more than 20 percent of your Kentucky Adjusted

Gross Income, or

you gave gifts of property that increased in value, made

bargain sales to charity, or gave gifts of the use of

property,

you expect to receive any state or local tax credit for a

contribution made.

You MAY NOT Deduct as Contributions

Travel expenses (including meals and lodging) while away

from home unless there was no significant element of

personal pleasure, recreation or vacation in the travel.

Political contributions.

Dues, fees or bills paid to country clubs, lodges, fraternal

orders or similar groups.

Value of any benefit, such as food, entertainment or

merchandise that you received in connection with a

contribution to a charitable organization.

Cost of raffle, bingo or lottery tickets.

Cost of tuition.

Value of your time or service.

Value of blood given to a blood bank.

The transfer of a future interest in tangible personal

property (generally, until the entire interest has been

transferred).

Gifts to:

Individuals.

Foreign organizations.

Groups that are run for personal profit.

Groups whose purpose is to lobby for changes in the

laws.

Civic leagues, social and sports clubs, labor unions and

chambers of commerce.

Contributions for which you receive any state or local

tax credit of more than 15% of the contribution.

Line 7—Enter all of your contributions paid by cash or check

(including out-of-pocket expenses).

Line 8—Enter your contributions of property. If you gave used

items, such as clothing or furniture, deduct their fair market

value at the time you gave them. Fair market value is what

a willing buyer would pay a willing seller when neither has

to buy or sell and both are aware of the conditions of the

sale. If your total deduction for gifts of property is more than

$500, you must complete and enclose federal Form 8283,

Noncash Charitable Contributions. If your total deduction is

over $5,000, you may also have to obtain appraisals of the

values of the donated property. See federal Form 8283 and

its instructions for details.

Page 5 of 5

Also include the value of a leasehold interest property

contributed to a charitable organization to provide temporary

housing for the homeless. Enclose Schedule HH.

Recordkeeping—If you gave property, you should keep a

receipt or written statement from the organization you gave

the property to, or a reliable written record, that shows the

organization’s name and address, the date and location of the

gift and a description of the property. You should also keep

reliable written records for each gift of property that include

the following information:

(a) How you figured the property’s value at the time you

gave it. (If the value was determined by an appraisal,

you should also keep a signed copy of the appraisal.)

(b) The cost or other basis of the property if you must reduce

it by any ordinary income or capital gain that would have

resulted if the property had been sold at its fair market

value.

(c) How you figured your deduction if you chose to reduce

your deduction for gifts of capital gain property.

(d) Any conditions attached to the gift.

(e) If the gift was a “qualified conservation contribution”

under IRC Section 170(h), the fair market value of the

underlying property before and after the gift, the type

of legal interest donated and the conservation purpose

furthered by the gift.

Line 9—Enter artistic charitable contributions. A deduction

is allowed for “qualified artistic charitable contributions” of

any literary, musical, artistic or scholarly composition, letter

or memorandum, or similar property.

An amount equal to the fair market value of the property on

the date contributed is allowable as a deduction. However, the

deduction is limited to the amount of the taxpayer’s artistic

adjusted gross income for the taxable year.

The following requirements for a deduction must be met:

(a) The property must have been created by the personal

efforts of the taxpayer at least one year prior to the

date contributed. The creation of this property cannot

be related to the performance of duties while an officer

or employee of the United States, any state or political

subdivision thereof.

(b) A written appraisal of the fair market value of the

contributed property must be made by a qualified

independent appraiser within one year of the date

of the contribution. A copy of the appraisal must be

enclosed with the tax return.

(c) The contribution must be made to a qualified organization

as described in this section.

Line 10—Enter any carryover of contributions that you

were not able to deduct in an earlier year because they

exceeded your adjusted gross income limit. See federal

Publication 526 for details on how to figure your carryover.

Line 12, Gambling Losses—You may deduct gambling losses

to the extent of your winnings reported on Form 1040 or

1040-SR, Schedule 1, line 8(b).

Line 13—Other Miscellaneous Deductions

Use this line to report miscellaneous deductions. Only the

expenses listed below can be deducted on line 13.

Federal estate tax on income in respect of a decedent.

Amortizable bond premium on bonds acquired before

October 23, 1986.

Deduction for repayment of amounts under a claim of

right if more than $3,000. See federal Publication 525.

Unrecovered investment in a pension.

List the type and amount of each expense. Enter one total on

line 13. For more information on these expenses, see federal

Publication 529.

Line 15—Total Itemized Deductions

Dividing Deductions Between Spouses—Married taxpayers

who are filing separate returns or a combined return

but using only one Schedule A must divide the itemized

deductions. Complete lines 16 through 20. If one spouse is

not required to file a Kentucky return, total deductions may

be divided between them based on the percentage of each

spouse’s income to total income or separate Schedules A

may be filed.